Spanish CNMC just released recently the 2022 Spanish Telecommunications Report

https://www.cnmc.es/sites/default/files/4807231.pdf

Let us go into relevant MVNOs details:

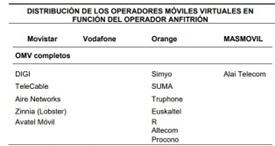

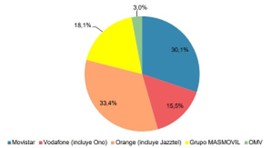

In 2022, MVNOs’ Spanish market share was 9.1% (total fleet of mobile lines), with 28 active MVNOs. The tables below show the map of the MVNOs assets in the Spanish market distributed according to the operator that provides access to the mobile network.

MVNOs figures do not include Tuenti, ONO, Lowi, Lycamobile, and Jazztel as all of them have been fully integrated into the corporate structure of their parent companies, disappearing as active MVNOs.

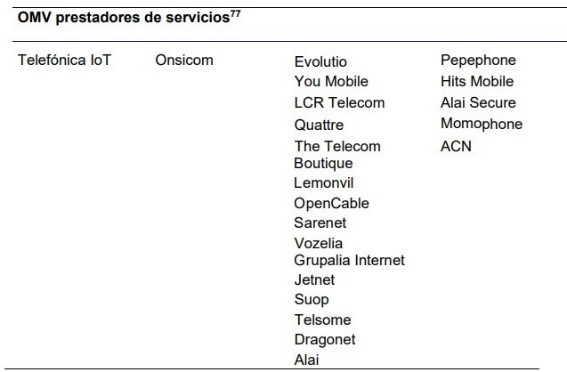

On the other hand, the market share percentage does not include Telefónica IoT, Simyo, Euskaltel, R, Telecable y Pepephone since these are operators owned by Movistar, Orange, and Grupo MÁSMOVIL respectively.

MVNOs distribution per host operator is as described in the following table:

A quick analysis shows that Vodafone and MasMovil strategies seem to not include Full MVNOs integration, but we can find several white brands under such operators.

Let’s continue with key facts, incomes and evolution, increase or decrease depending on the type of MVNO:

Specifically, the service of access to mobile communication networks by third parties operators, mainly MVNOs, recorded a 5.5% increase in its billing, obtaining a total income of 781.1 million euros.

It is convenient to disaggregate this turnover based on the ownership of the MVNO to which the MNO provided the access service. If we analyze the access service provided to MVNOs not owned by network operators, it can be seen that revenues increased by a significant 14.6% compared to the figure billed the previous year.

As regards the income related to the access services that the OMRs lent to their

MVNOs, these fell by 8.8%, mainly due to the cessation of the activity of some of these operators as OMV itself and the consequent integration of these within the internal structure of the MNO.

In 2022, this was the case for the MVNO Lowi and Lycamobile, which were integrated into the operators Vodafone and Grupo MASMOVIL respectively.

Revenues from the national mobile voice termination service registered a significant year-on-year drop of 21%. The fall in 2022 would be explained, in large part, by a fall in the maximum termination price.

All the contrary about the international roaming service. This service registered an overall increase in revenue of 43.5% year-on-year and this increase was located especially in the data service.

Above figures clearly show how important is to achieve good outbound roaming agreements, steering of roaming capabilities, and eSIM to build a nice offer for travelers and roamers-in for MVNOs.

Finally, wholesale income concentration is traditionally higher than that observed in the retail market. The main reason for that is that generally MVNOs do not have their infrastructure and, therefore, their interconnection traffic concentrates on the networks of the MNOs who, in return, receive economic compensation.

To summarize, there is still room for growth as mobile telecommunications services are on a continuous rise, and new 5G technology (do not miss the next blog entrance for 5G Spanish deployment analysis) is still in its early days.