Disclaimer: This article does not aim to question any of the offers analyzed, nor has it been sponsored by any of the mentioned (or unmentioned) operators. It is the result of an analysis from the perspective of a consulting professional who needs to understand the market and its trends. However, if any of the operators mentioned detect an error in our information or have comments to add, please do not hesitate to contact us. We will be happy to review and modify it.

Introduction

In the first part of this Guest Blog the Spanish Mobile Market was analyzed, the second Guest Blog illustrate how MVNO’s are distributed in the Market. This third part is about the rates, costs and data.

As expected, the third part of this analysis has taken much longer than anticipated, and even more than desired. To complete this work, I have had the valuable collaboration of Pedro Pascual, who has devoted a considerable number of hours reviewing the offers from both network and virtual mobile operators in Spain.

Rates, Costs and Data

The rates presented in this blog, as well as their costs, are likely to be valid for only a few weeks. The importance of the article lies in the analysis of the differences between the offers available in the market and their prices, rather than the specific cost or value of each gigabyte of data we can access from our mobile devices.

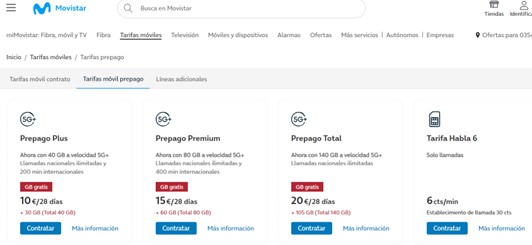

It should be noted that we have analysed contract-based rates, although, as we will see in this blog, we do mention a few prepaid rates due to their surprising prices.

Although we have not analysed all the more than 900 virtual mobile operators in their various forms, we have reviewed the offers from several hundred. Nevertheless, we will begin our analysis with “Full” virtual mobile operators, i.e., those registered with the AOPM. Later, we will extend the analysis and, of course, the conclusions to the rest of the operators reviewed. From this list, we have excluded operators that focus exclusively on IoT (Internet of Things), as well as some enablers that do not offer services to end-users, such as citelia, siptize or suma móvil, the enabler for Orange.

We found other cases, such as Avatel Telecom or Fibritel (an OMV dependent on Aire Networks), where there is no standalone mobile service offer; it must always be combined with a fiber offer.

As expected, the analysis has focused solely on mobile services, although we have also noted for all operators whether they offer additional services besides mobile telephony, such as fiber offers, convergent offers, business offers, or if their focus is purely residential.

Among the 39 operators analyzed, we found 108 mobile-only rates, which are curiously distributed across 34 different offers.

Perhaps calling them different offers is a bit bold. Should I say they are distributed across 34 identical offers with varying amounts of data? This is the first aspect I want to draw attention to. After analyzing dozens or hundreds of operators, there is practically no difference in their service offerings. It’s a matter of adding or subtracting a few more gigabytes for a few less cents.

Lowest amount of Data and Cheapest

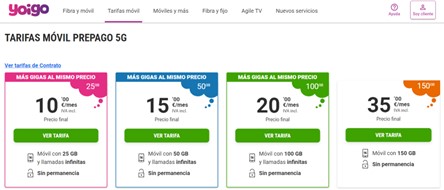

Yoigo

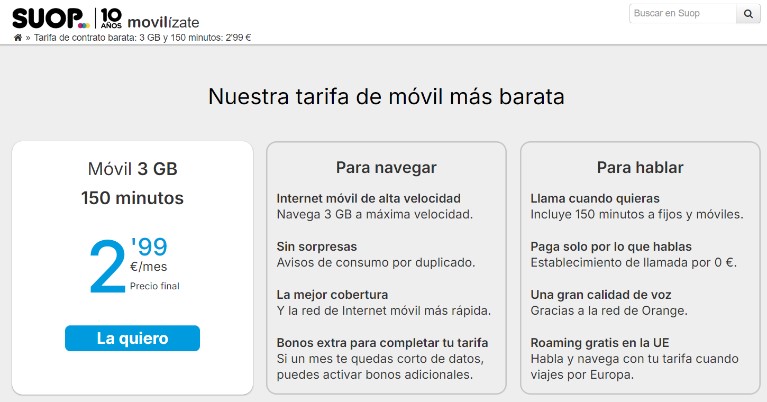

The rate with the lowest amount of data found corresponds to a 500-megabyte rate from Yoigo, which, however, is not the most economical.

Simyo

Although one could say that Simyo is close behind with an offer of 5 euros for 4 GB

Sarenet

Sarenet, an operator specialized in businesses, offers a mobile-only plan with 4 GB for just €6, although they offer 3€ with a 50% discount for the first few months.

Big Amount of Data

On the opposite end, in terms of the amount of data available monthly, we found a whopping 15 offers among the 39 full MVNOs analyzed, with prices ranging from €8.33 per month to €39.90.

Aló – Esdomo Telecom

Without a doubt, we were surprised by the offer from Aló, a commercial brand of Esdomo Telecom, where our good friend Thorsten Bergmann introduces a feature that is not very common in the Spanish market: annual payment for services, which crowns it as the most economical unlimited offer on the market.

During this analysis, one thing that particularly caught our attention was the variety in the amount of data offered by operators. Most of these offers, following a mathematical logic of simplicity, are multiples of 5 or 10 (haha, of course, if it’s a multiple of 10, it’s also a multiple of 5 😊). However, we also found some rather interesting options.

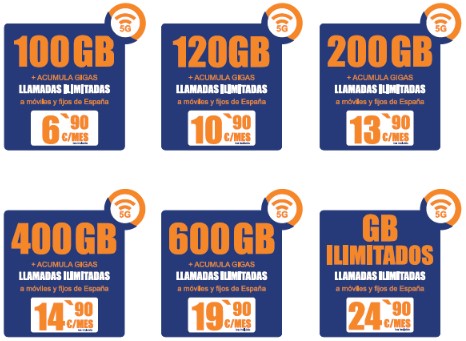

Lemonvil

Regarding 5G we could highlight Lemonvil, which positions itself as the first virtual mobile operator in Spain with 5G.

And its aggressive offering with 10GB just for 6,90€ or unlimited for 24,90€.

An important point to highlight in this case is the condition included in these offers regarding data usage control. It is clearly specified that an analysis of the type of device used will be carried out.

“To ensure that you always have the best quality, we do not allow the use of SIM cards in routers, modems, or other traffic aggregation devices, nor their use for sharing data 24 hours a day or most of the time”. Very good point!!

And in this context, what is the position of mobile operators with access networks?

If we take a look at the table of mobile-only offers (let’s not forget that this analysis focused on mobile-only rates and the vast competition we find), the offers from operators with access networks (OMRs) do not differ significantly, as we can see below:

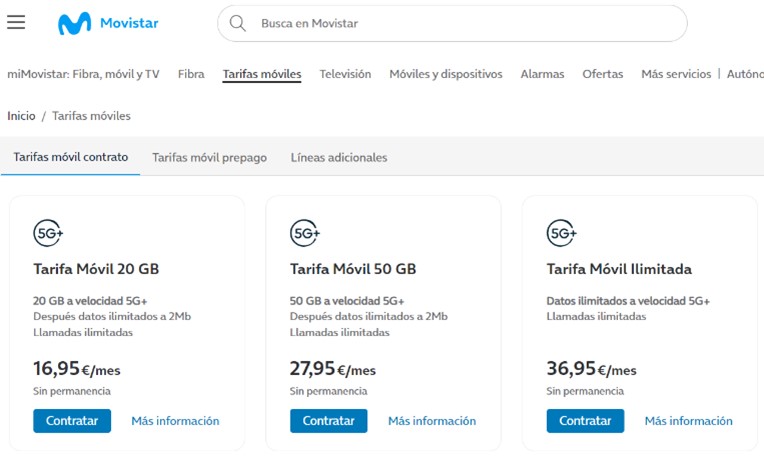

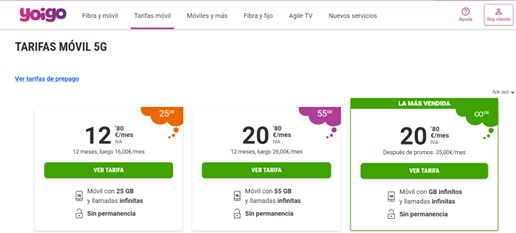

Movistar

All of them focus on rates that include 50 GB and unlimited data, with Movistar being the operator with the highest rates in those segments. Voice has had no value for some time now (infinite or unlimited calls, but be careful with roaming outside the EU) and there is no contract commitment.

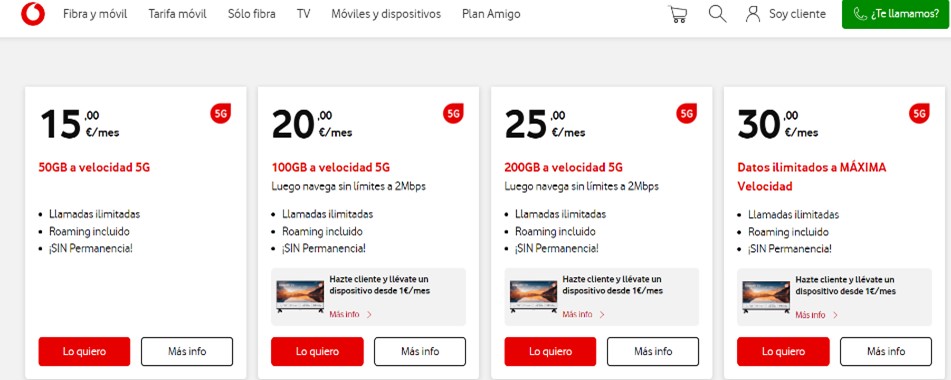

Vodafone

We can see that Vodafone is directly targeting plans with a larger amount of gigabytes.

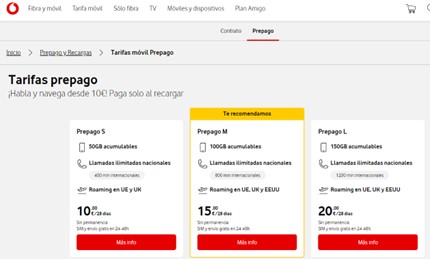

Be careful; we might be surprised. There are prepaid rates that are even cheaper than contract rates, with no commitment periods and no significant differences in usage. This could be a clue for new MVNOs (though one must consider the cost of the necessary charging infrastructure to manage prepaid services).

Dragonet

We also cannot overlook some of the surprises we encountered, such as with Dragonet, where a super aggressive rate is announced

And yet, as we progressed through the contracting process, we encountered prices significantly higher than those advertised on their main page. We assume this is either an error or that it hasn’t been updated correctly:

We haven’t gone through this process with all the operators analyzed, but it is an aspect to consider if we want Happy Customers, Happy Business: The Recipe for Success, as we mentioned in the first of our blogs. After all, billing errors are one of the main causes of dissatisfaction.

The importance of knowing all these retail offers we have found in the market is ultimately to understand the market when creating our business case and negotiating wholesale agreements with the host operator.

How should wholesale prices be structured to compete under reasonable conditions with access network providers?

It is well known that the success of a business that buys gigabytes and minutes at wholesale largely depends on a good statistical analysis of service usage by the mobile operator’s users. A miscalculation can lead to astronomical payments to the host of the virtual mobile operator, while recurring revenues may fall below the actual cost.

What we can analyze in this scenario is the minimum, maximum, and average prices that operators are managing overall. It should be noted that, although all analyzed operators offer unlimited calls, in wholesale negotiations, we will encounter costs for calls and messages.

Thus, for the most common rates (those that appear most frequently), we would have: 10 GB starting from €5.90 with Finetwork (in this case, we have verified that there is no price variation in the initial stages of contracting, which we clearly have not completed), up to €9 with Euskaltel (we have seen some much higher rates, but undoubtedly they are the result of an outdated or even forgotten offer). We see that the price per gigabyte would be between €0.590/G and €0.900/G, but let’s look at some more generous offers in gigabytes.

If we jump to 30 GB, of which we found 9 offers solely among the operators of the AOPM, we would have the offer of €7.95 from Procono (PTV telecom.com) that recently made headlines for signing with Vodafone (which gives us an idea, along with Finetwork’s offer, of the aggressiveness in pricing). On the other hand, we see Euskaltel again positioning itself at the higher end of the price spectrum with an offer of €16.

The price range per gigabyte is now much more reasonable, between €0.265/G and €0.533/G.

If we see 100GB from previous mentioned Lemonvil offer, or its 400GB and 600GB, you see that we are in ranges of 0,069 €/G in the firs case, and just 0,037 €/G and 0,033 €/G for the last ones… Just 3,3 cents per Gigabyte!

To avoid extending this further, as this entry has become a bit lengthy, let’s quickly analyze the offers for 200 GB, where the champion is Digi at €16, or €10 if you sign up for fiber. This means the resulting price is €0.080/G (€0.050/G if combined with fiber—just 5 cents!). On the other end, we have Youmobile at €0.175/G (I must admit that this offer includes an unlimited calling package to China, as Youmobile is the Spanish operator specialized in the Chinese community).

Summarizing, that it is a gerund (Spanish expression):

We can summarize this entire analysis into two fundamental points:

- The mobile-only offer, which most MVNOs can aspire to without entering the complexity of combined offers with fibre, is largely a competition to see who offers the most gigabytes at the lowest price.

- There are some differentiated offers aimed at businesses or very specific niches where the mobile service offering becomes a necessity that could be considered defensive.

- Beyond the mobile service, we find cross-selling with fibre, TV services, and in some cases, the sale of devices, as well as some security services or utility services. From our point of view, there is nothing truly innovative; although some proposals require very advanced business support systems (BSS) if they want to consolidate cross-offers.

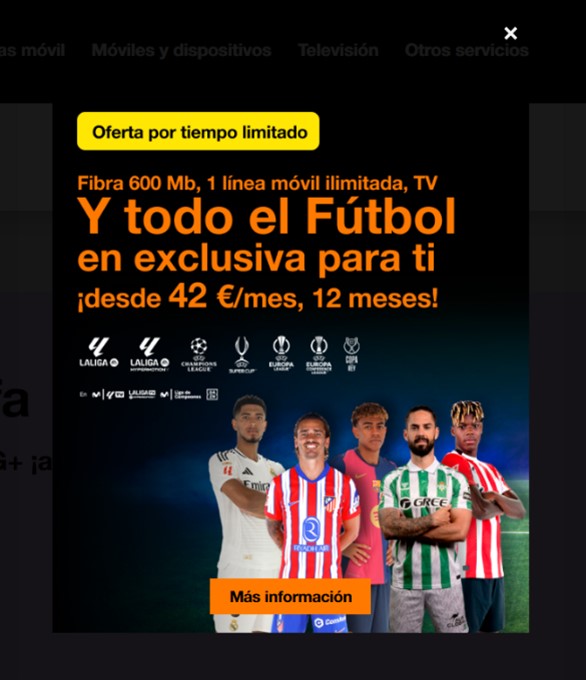

Finally, we cannot overlook some curiosities that will lead us into the last part of the study about the future of MVNO services. For instance, in the case of Orange, we noticed that with every step we took on their website, a popup about football appeared… everything is football, or should we say, is everything football?

That’s not all folks

Don’t miss the next and final installment (Part IV), where we want to analyze what other services and models are offered by MVNOs outside of Spain.

We will see you in the next chapter.